“Are We Approaching a Historic Bear Market? Henrik Zeberg Thinks So — Here’s Why”

Introduction

Henrik Zeberg, a prominent market analyst known for his bold predictions, has issued a stark warning: we may be on the verge of the biggest recession and bear market since the Great Depression of 1929. According to Zeberg, markets are inching closer to a final peak, a tipping point that could trigger a massive downturn. In his analysis, Zeberg delves into the alarming rise in unemployment, the looming recession, and persistent inflation — factors he believes are converging to form a perfect Bear Market.

Elliott Wave

According to Henrik Zeberg, we’re in the midst of the biggest economic bubble in history, and there are clear signals that the market is now reaching a crucial turning point. While many thought the economy was starting to slow down in 2022, Zeberg believes that shift is only beginning now, with telltale signs across global markets. He emphasizes that we’re seeing a euphoric rise in asset values — a typical behavior at the peak of business cycles, just before the downturn.

One of the key tools in Zeberg’s analysis is the Elliott Wave Theory, a technical approach used to forecast market trends by identifying repeating patterns or “waves.” According to this theory, markets move in cycles of upward and downward waves, and Zeberg believes we may be reaching the end of an extensive upward cycle.

In addition to the Elliott Wave Theory, Zeberg points to Fibonacci levels — a method that uses mathematical ratios to predict support and resistance levels in markets, are been hit on the Dow Jones index, a key indicator that a market top could be close. Furthermore, he points out that certain technical indicators, like divergences, are appearing across markets such as the S&P 500, NASDAQ, and even international indexes like Japan’s Nikkei and India’s Nifty. A divergence happens when the price of an asset rises, but the momentum (or trading volume and investor enthusiasm) behind it weakens. This suggests a lack of underlying strength, often seen before a market reversal.

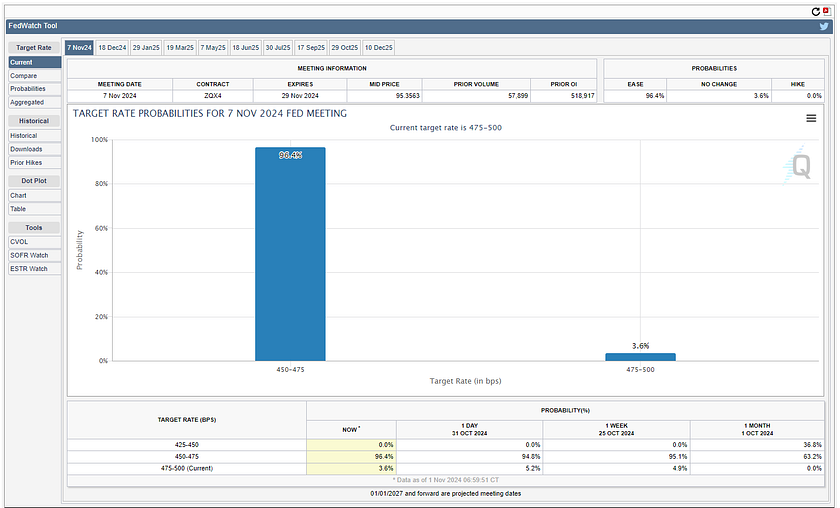

FED and Elections

Eight months ago, Zeberg argued that the Federal Reserve should have halted its rate hikes, as their extended “hawkish” stance has placed excessive pressure on the economy. This approach, coupled with pandemic-era stimulus measures, has triggered a series of negative consequences. Specifically, rising inflation has driven up yields, ultimately straining the business cycle and creating a precarious economic environment.

Amid these challenges, the real issue lies with everyday Americans — families grappling with job losses, mounting debt, and the strain of higher interest rates on mortgages and loans. While financial markets often dominate the headlines, Zeberg emphasizes that the true economy — one that directly impacts households and consumers — is what truly matters in assessing economic health.

In addition to these economic factors, Zeberg addresses the political climate and its potential impact on markets. He notes that election outcomes could lead to short-lived boosts, particularly in sectors like cryptocurrency. For instance, if Donald Trump were to win the election, it might generate a temporary wave of optimism for crypto assets. However, he believes these effects would be fleeting; ultimately, the overall health of the economy relies more on fundamental factors than on political changes.

Looking ahead, Zeberg warns that if the Fed fails to adjust its approach soon, we could face a looming deflationary cycle where consumers hold back on spending, leading to further economic decline. In this scenario, even if the Fed attempts to intervene, the downward spiral may already be in motion — something Zeberg believes we are currently witnessing.

NAHB Housing Index

In the current economic cycle, a fundamentally broken structure exists that neither the Treasury nor the Federal Reserve has been able to repair: the housing market. The decision to allow the housing market to collapse has resulted in dire consequences for the overall economy.

When examining the National Association of Home Builders (NAHB) housing market index, a clear pattern emerges: each time interest rates rise, the housing market takes a hit. This decline is closely linked to a rise in unemployment, highlighting the interconnectedness of these economic factors.

As the economy deteriorates, there is often a lag before the effects are fully felt across different sectors. This delay was evident during the financial crisis, where a significant period passed before unemployment rates peaked. Observing current trends, it raises important questions about the trajectory of the housing market and the broader economy moving forward.

Soft Landing

When discussing the concept of a “soft landing,” it’s important to consider how it has historically been associated with the Federal Reserve’s actions during economic transitions. A soft landing refers to a scenario where the economy slows down gradually without falling into a recession. Typically, this occurs when the Fed cuts interest rates to stimulate growth, as evidenced by past instances where the Fed successfully navigated this transition.

In analysing the current economic landscape, it’s critical to look at the relationship between the Fed funds rate and two-year yields. In previous soft landing scenarios, when the Fed cut rates, we often did not see a recession, primarily because economic indicators, such as unemployment, did not flash warning signs. For instance, unemployment rates continued to decline without showing signs of inversion in the yield curve, which typically signals economic distress.

Yield inversion occurs when shorter-term interest rates exceed longer-term rates, suggesting that investors expect economic slowdown. In this case, if the two-year yield surpasses the ten-year yield, it indicates a lack of confidence in the short-term economic outlook. Historically, yield inversions have signaled impending recessions, and currently, we are witnessing one of the most significant yield inversions on record — greater than those seen in 1929 and 2007. According to market analyst Henrik Zeberg, this unprecedented yield inversion raises serious concerns about the stability of the current economic environment.

This significant yield inversion is troubling, especially when considering the current market dynamics. With market capitalization to GDP now at an astonishing 200%, this far exceeds the 107% seen in 2007 and the 129% during the dot-com bubble in 2000.

Furthermore, continuous jobless claims are also trending upward, mirroring patterns seen before past recessions. Structural unemployment figures indicate that the duration of unemployment is historically high, suggesting that individuals are remaining jobless for longer periods — a telltale sign of an economic slowdown.

These indicators collectively present a troubling picture: the business cycle is rolling over, and we are receiving recession signals similar to those observed in previous downturns. As noted by Zeberg, with the combination of high valuations and deteriorating economic indicators, the question arises: can we truly expect a soft landing when the underlying economic signals point toward a more serious deterioration?

Final Thoughts

Despite the broader economic uncertainties, Zeberg remains bullish on Bitcoin, expressing confidence in its potential to reach a target range between $115,000 and $123,000. He notes, “I have a target for Bitcoin that has stood for quite some time. I believe it’s going to develop very quickly, and it will happen soon. In the next few days, I think we will see an all-time high and that it will blow right past it.” While I personally have a more conservative outlook — anticipating Bitcoin to hit around $100,000 — I share his optimism regarding the cryptocurrency’s upward momentum.

Zeberg also emphasizes the importance of the dollar’s trajectory in this context. He believes the dollar is set to decline significantly, projecting levels between 95 to 97 on the DXY index. He warns that as the dollar bottoms out, we may experience a “deflationary bust of a lifetime,” which could adversely impact a wide range of assets, including cryptocurrencies and stocks.

Additionally, he highlights a noteworthy trend: market rotation. Zeberg points out that during the final phase of a business cycle, money often shifts from foreign markets to perceived safe havens like the U.S. market. This rotation is typical during periods of economic slowdown, as investors seek stability.

In conclusion, we will see a significant market peak within the next six months, followed by a major crash.

Index of Terms

- DXY (U.S. Dollar Index): A measure of the value of the United States dollar relative to a basket of foreign currencies. A decline in the DXY indicates a weakening dollar, which can impact international trade and investments.

- GDP (Gross Domestic Product): The total monetary value of all goods and services produced within a country over a specified period, often used as an indicator of a country’s economic health and performance.

- NAHB Housing Market Index: An index measuring builder and developer sentiment in the residential real estate market. A higher index indicates a more positive outlook on home sales and construction activity.

- NASDAQ: A global electronic marketplace for buying and selling securities, known for its high concentration of technology and growth-oriented companies. The NASDAQ Composite is a stock market index that includes over 3,000 stocks listed on the NASDAQ stock exchange.

- Fibonacci Levels: A technical analysis tool that uses mathematical ratios derived from the Fibonacci sequence to identify potential support and resistance levels in financial markets.

- Yield Inversion: A phenomenon where short-term interest rates exceed long-term rates, indicating that investors expect economic slowdown. This inversion is often viewed as a precursor to recessions.

- Job Market: The arena in which employers seek employees and job seekers search for employment. Factors such as unemployment rates, job growth, and wage levels are critical indicators of a healthy job market.

- Wage Levels: The average amount of compensation (salaries, wages, bonuses, etc.) paid to workers for their labor. Wage levels are critical indicators of economic health and can influence consumer spending, inflation rates, and overall economic growth. Changes in wage levels can impact labor supply and demand, affect businesses’ profitability, and influence monetary policy decisions made by central banks.

- Piper Sandler Recession Indicator: A tool developed by Piper Sandler, a financial services firm, which uses a combination of economic data and trends to predict the likelihood of an impending recession. This indicator analyses various metrics, such as employment rates, consumer spending, and manufacturing activity, to gauge the overall health of the economy.

Leave a Reply